The Real Cost of Probate in Maryland

Ron Swanson would probably hate estate planning.

Not because he hates his family.

Not because he is irresponsible.

And certainly not because he is afraid of death.

Ron Swanson is not afraid of death. Death is probably afraid of Ron Swanson.

But if you know the character from Parks and Recreation, you can almost hear him saying something like this:

“I do not need a lawyer to tell me what happens to my property when I die. I own my house. I own my tools. I own my meat freezer. My family can figure it out.”

That attitude is funny on television. In real life, it can become expensive.

And unfortunately, I meet versions of this attitude all the time.

Usually, it sounds something like:

- “I do not need anything complicated.”

- “My wife will get everything anyway.”

- “My kids know what I want.”

- “I do not want to pay for documents I may never use.”

- “I am not rich enough for estate planning.”

I understand the instinct.

Most people do not wake up excited to spend money on wills, trusts, powers of attorney, beneficiary designations, and legal documents. Estate planning is not a new toy. It is not a vacation. It is not a truck. It is paperwork about things no one really wants to think about.

But here is the mistake:

Avoiding estate planning usually does not avoid the cost.

It just moves the cost to your family after you are gone.

And by then, the person (i.e., you) who could have made everything easier is no longer available to answer questions. And so now you have made it more difficult, more expensive, and more time-consuming that it needed to be, and why?

“My Family Will Figure It Out”

This is one of the most common assumptions in estate planning.

And in fairness, many families do eventually figure it out.

But “eventually” can involve a lot of time, stress, confusion, paperwork, and expense.

When someone dies owning assets in his or her individual name, the family may need to open a probate estate. That usually means someone has to be appointed by the court as personal representative. The personal representative then has legal duties to identify assets, notify interested persons, deal with creditors, file inventories and accountings, manage estate property, and ultimately distribute what remains.

That may sound manageable in theory.

In practice, it often begins with a scavenger hunt.

- Where is the will?

- Is there a newer will?

- Who has the original?

- Where are the bank accounts?

- Is there life insurance?

- Who are the beneficiaries?

- Is the house titled jointly or individually?

- Are there retirement accounts?

- Did Dad have a safe deposit box?

- What bills are still being paid automatically?

- Where are the passwords?

- Who gets the truck?

- Why is there a random envelope from 2014 labeled “important”?

This is where the “my family will figure it out” plan starts to show its weaknesses.

Your family may be grieving.

They may not know what you owned.

They may not know who to call.

They may not know whether your accounts have beneficiary designations.

They may not know whether your old will is still valid.

They may not know whether your real estate has to go through probate.

And even if everyone gets along, they still have to follow the legal process.

The Cost Is Not Just Money

When people ask about the cost of estate planning, they usually mean attorney’s fees.

That is fair. Cost matters.

But when comparing the cost of estate planning to the cost of probate, you have to look at the whole picture.

Probate can involve court costs, attorney’s fees, personal representative commissions, bond premiums, appraisal fees, accounting fees, publication costs, tax filings, real estate expenses, and other administrative costs.

Some estates are simple. Some are not.

A modest estate with clean records, cooperative beneficiaries, and properly titled assets may move relatively smoothly. A disorganized estate with missing documents, outdated beneficiaries, real estate issues, family tension, or unclear instructions can become much more expensive and time-consuming.

This is especially frustrating because many of those problems are preventable.

A well-designed estate plan does not guarantee that nothing will ever be difficult. Life is still life. Families are still families. Assets change. Laws change. People change.

But a good plan can reduce confusion.

It can identify who is in charge.

It can waive bond where appropriate.

It can keep certain assets out of probate.

It can coordinate beneficiary designations.

It can provide instructions for incapacity and death.

It can tell your family where things are and what you wanted.

Most importantly, it can keep your loved ones from having to solve a legal puzzle at the worst possible time.

The Ron Swanson Problem

The Ron Swanson type of client is not foolish.

In fact, he is often very responsible.

He pays his bills.

He works hard.

He takes care of his house.

He changes his own oil.

He owns tools for situations most people do not know exist.

He does not like being upsold.

He does not like unnecessary meetings.

He does not want to pay someone to make a simple thing complicated.

Honestly, I respect all of that.

But estate planning is not about making simple things complicated.

It is about keeping complicated things from becoming worse.

The person who says, “I do not want to pay for estate planning,” is often trying to save money for the family.

But without realizing it, he may be doing the opposite.

He may be leaving his spouse or children with more legal work, more delay, more uncertainty, and more expense than necessary.

That is not frugal.

That is deferred maintenance.

And deferred maintenance almost always costs more.

Anyone who has ignored a small leak, a weird engine noise, or a roof problem knows exactly how this works.

The cheap option today can become the expensive option later.

Estate planning is similar.

You can deal with certain issues while you are alive, healthy, and able to make decisions.

Or your family can deal with them after you are gone, when they are grieving, under pressure, and trying to reconstruct your financial life from bank statements, old mail, and whatever they can find in your desk drawer.

Probate Is Not Always Bad

To be clear, probate is not some villain lurking in the shadows.

Maryland probate exists for a reason.

It provides a legal process for transferring property, paying creditors, protecting beneficiaries, and making sure estates are handled properly.

Sometimes probate is necessary.

Sometimes probate is not especially difficult.

And sometimes a simple will-based plan is perfectly appropriate.

The point is not that every person needs an elaborate trust.

The point is that every person should understand what will happen if they do nothing.

Because doing nothing is still a plan.

It is just a plan where Maryland law, court procedures, account titles, beneficiary forms, and whatever documents your family can find will determine what happens next.

That may work out fine.

Or it may not.

“But Everything Goes to My Wife”

This is another common assumption.

Many married people believe that if one spouse dies, everything automatically goes to the surviving spouse.

Sometimes that is true.

Sometimes it is not.

It depends on how assets are titled, whether beneficiary designations are in place, whether there is a valid will, whether there are children from another relationship, whether accounts are jointly owned, and what kind of property is involved.

Even when the surviving spouse ultimately receives everything, there may still be work required to get there.

A spouse may need to open an estate.

A spouse may need to be appointed personal representative.

A spouse may need to deal with banks, title companies, creditors, appraisers, tax filings, and court paperwork.

That is not nothing.

And if the surviving spouse was not the one who handled the finances during the marriage, the process can be even more stressful.

This is one reason I often see one spouse more engaged in estate planning than the other.

Many times, the wife understands the practical reality immediately.

She knows who will be making the calls.

She knows who will be looking for documents.

She knows who will be trying to figure out what the accounts are, what bills are due, where the passwords are, and what steps need to be taken.

She is not thinking about estate planning as an abstract legal exercise.

She is thinking:

“Please do not leave this mess for me.”

That is a very reasonable request.

The Real Cost of Waiting

The real cost of probate is not just the check written to the lawyer.

It is the time.

The delay.

The uncertainty.

The missed work.

The family tension.

The court filings.

The appraisals.

The bond issue.

The tax questions.

The house that cannot be sold as quickly as expected.

The account no one can access.

The beneficiary form that was never updated.

The family member who thought there was a different plan.

The surviving spouse sitting at the kitchen table trying to make sense of documents that should have been organized years earlier.

Estate planning is not really about death.

It is about responsibility.

It is about taking the time now to make things easier later.

It is about not leaving your loved ones with a scavenger hunt.

It is about not forcing them to pay, wait, guess, and search because you did not want to sit down and make a plan.

A Better Kind of Frugal

There is nothing wrong with being careful about money.

In fact, good estate planning should respect that.

Not every family needs the same plan. Not every family needs a trust. Not every family needs complex tax planning.

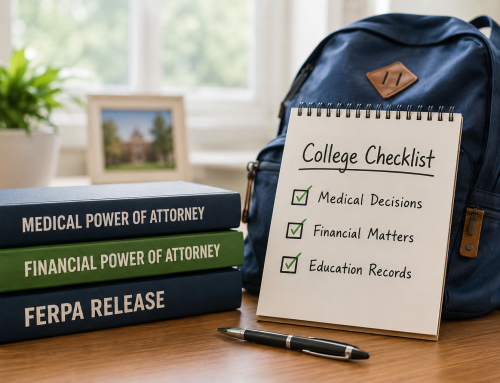

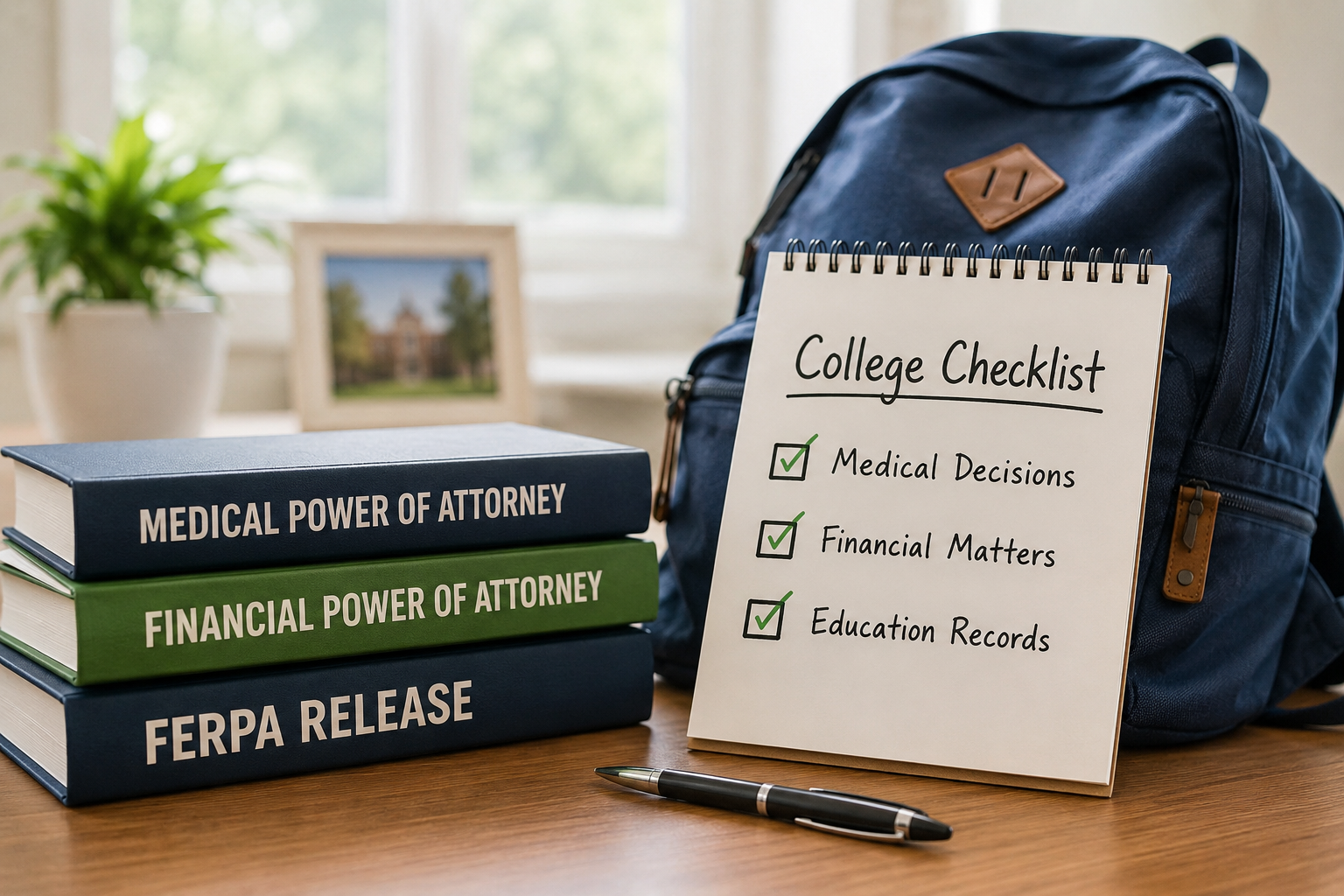

But most adults should have at least a basic plan that addresses the major questions:

Who can make financial decisions if I am incapacitated?

Who can make medical decisions if I cannot speak for myself?

Who handles my estate when I die?

Who receives my property?

Are my beneficiary designations current?

Will my family know where to find important information?

Can anything be done now to reduce unnecessary probate costs later?

These are not exotic questions.

They are practical questions.

Ron Swanson might not enjoy the meeting.

He might not like the paperwork.

He might stare suspiciously at the printer.

But he would understand the principle:

Do the job right the first time.

Because when it comes to estate planning, the cheapest plan is not always the one that costs the least today.

Sometimes the cheapest plan is the one that saves your family from a much bigger mess tomorrow.

Final Thoughts

Probate in Maryland can be manageable, but it is rarely something your family wants to learn from scratch while grieving.

A thoughtful estate plan can help reduce confusion, avoid unnecessary costs, and give your loved ones a clearer path forward.

Avoiding estate planning does not make the legal issues disappear.

It simply leaves them for someone else.

And that someone else is usually the person you most wanted to protect.

If you have been putting off your estate plan because you think you are saving money, it may be time to take a closer look.

You may not be avoiding the cost.

You may just be leaving the bill, the paperwork, and the scavenger hunt for your family.

Clarity is cheaper than chaos.

And it is a much better gift to leave behind.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave A Comment