What If Luke Skywalker Had Inherited a Million Credits?

Luke Skywalker lost his parents as an infant.

Fortunately, he had Uncle Owen and Aunt Beru.

They gave him a home.

They put food on the table.

They raised him as their own.

And they did their best—unsuccessfully, as it turned out—to keep him away from dangerous ideas involving old Jedi Knights, lightsabers, and galactic rebellions.

But let’s imagine a question that Star Wars never answered:

What if Luke’s parents had left him a million credits?

Who would have controlled the money?

Would Uncle Owen and Aunt Beru have been able to access it to pay for Luke’s clothes, education, transportation, and daily needs?

Or would someone else have been responsible for managing those funds?

As strange as it sounds, this is a real estate planning issue that parents face every day.

When parents with young children create an estate plan, they often focus on one important question:

“Who would raise my children if something happened to me?”

But there is a second question that is just as important:

“Who would control the money?”

The Guardian and the Trustee Are Not Always the Same Person

Most parents assume that the person raising their children would automatically control the children’s inheritance.

That is not necessarily true.

In many estate plans, parents intentionally separate those responsibilities.

One person serves as Guardian, responsible for raising the children.

Another person serves as Trustee, responsible for managing the money.

This arrangement often makes sense.

The guardian focuses on parenting.

The trustee focuses on financial management.

It also creates a system of checks and balances that can help protect the children’s inheritance.

But it can create practical challenges as well.

The guardian may be the one buying school supplies, paying for soccer registration, purchasing winter coats, arranging summer camps, and covering countless day-to-day expenses.

Meanwhile, the trustee controls the money.

The guardian may need to request distributions from the trustee, who must then decide whether the request falls within the terms of the trust.

Most of the time this works just fine.

But it highlights an important reality:

Estate planning is not just about who gets the money.

It is also about making sure the right people have access to the resources they need when they need them.

Enter the UTMA Account

One tool that families sometimes use to address this issue is a UTMA account.

UTMA stands for the Uniform Transfers to Minors Act.

In simple terms, a UTMA account allows money or property to be held for a child while an adult manages it on the child’s behalf.

The child owns the money.

The adult custodian manages it.

The custodian can use the funds for the child’s benefit until the child reaches the age established by law.

UTMA accounts are commonly used for:

- Gifts from parents and grandparents

- Investment accounts for children

- Smaller inheritances

- Life insurance proceeds payable to minors

- Savings intended for future educational expenses

They are generally simple to establish and can be opened through most banks and brokerage firms.

Why Some Families Like UTMA Accounts

The biggest advantage of a UTMA account is simplicity.

Suppose Grandma wants to leave $20,000 to her granddaughter.

Creating a separate trust may be unnecessary.

A UTMA account allows the money to be managed by a trusted adult until the child reaches adulthood.

Likewise, parents who want to invest money for a child may find a UTMA account to be an easy and cost-effective solution.

For modest amounts of money, a UTMA account can work very well.

The Catch

As with most things in estate planning, simplicity comes with tradeoffs.

Unlike a trust, a UTMA account offers limited flexibility.

Eventually, the custodianship ends and the child receives control of the account.

For some families, that is perfectly acceptable.

For others, it is not.

Many parents tell me:

“I love my child, but I’m not sure I want them receiving a large sum of money at age 18 or 21.”

That’s a fair concern.

Most of us can remember at least one questionable financial decision we made in our late teens or early twenties.

Some young adults are ready to manage substantial assets.

Others are not.

If controlling the timing of distributions is important, a trust may be the better option.

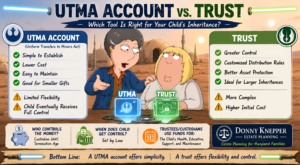

UTMA Accounts vs. Trusts

Both UTMA accounts and trusts can benefit children.

They simply accomplish different goals.

A UTMA Account May Be Better When:

- The amount involved is relatively modest

- Simplicity is important

- The donor is comfortable with the child eventually receiving control

- The goal is to make a straightforward gift

A Trust May Be Better When:

- The inheritance is substantial

- The donor wants to delay distributions

- Asset protection is important

- Detailed instructions are desired

- There are concerns regarding maturity, creditors, divorce, or special needs

A trust generally provides more control.

A UTMA account generally provides more simplicity.

Neither is automatically better.

The right answer depends on the family’s goals.

Back to Luke Skywalker

If Luke Skywalker had inherited a million credits, there is a good chance that Uncle Owen and Aunt Beru would have appreciated having access to at least some of those funds while raising him on Tatooine.

After all, moisture farming wasn’t exactly a path to unlimited wealth.

More importantly, Luke’s story highlights a question that every parent should consider:

If my children inherit money while they are still minors, who will manage it?

And perhaps even more importantly:

Will the people caring for my children have practical access to the resources they need?

Those questions deserve careful thought.

Because while most of us will never train with Obi-Wan Kenobi, battle Darth Vader, or help overthrow a Galactic Empire, every parent hopes their children will be protected and provided for if the unexpected happens.

Final Thoughts

Good estate planning is about more than documents.

It is about anticipating real-world challenges and creating practical solutions.

UTMA accounts are one of those tools that many families have never heard of, yet they can play an important role in the right circumstances.

For some families, they provide a simple and effective way to manage money for children.

For others, a trust may offer greater flexibility and protection.

The key is understanding the difference—and making sure your plan reflects what you actually want to happen.

Does This Affect Your Estate Plan?

If you have minor children, are considering creating a trust, or want to discuss the best way to leave money to children or grandchildren, now is a good time to review your plan.

A well-designed estate plan does more than distribute assets. It helps ensure that the people you trust have the resources and authority they need to care for the people you love most.

Contact our office today to schedule a consultation.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave A Comment